I. Overview of the First Half of 2011

Robert Khuzami, the Director of the Division of Enforcement (the “Division”) of the SEC, recently took stock of the SEC’s accomplishments in the two years since he began his term. Specifically, he focused on the Division’s restructuring, calling it the “most significant” since the Division’s creation almost 40 years ago.[1] In describing the restructuring, he noted that it was composed of many initiatives that were intended to achieve a series of common goals including: achieving a better understanding of the products, markets, transactions and practices policed by the Commission; identifying and terminating fraud and misconduct more quickly; increasing efficiency in the use of resources; and maximizing the Division’s deterrent impact by swiftly addressing threats as they develop and before they can permeate entire business lines or industries.[2]

In order to achieve these goals, this Commission is marked by a continued willingness to take on risk in litigation, particularly in cases related to insider trading and to extend jurisdiction and remedies. The last six months have seen some significant victories in the SEC’s litigation efforts and accordingly, we expect the SEC to continue to pursue an aggressive strategy of filing cases against prominent defendants to demonstrate its vigor in investor protection. Highlights of the past six months include:

- Finalizing the Whistleblower Rules of the Dodd-Frank Act;

- The first use of a deferred prosecution agreement;

- The first use of the authority granted under the Dodd-Frank Act to pursue penalties against unregistered persons in administrative proceedings;

- Continued emphasis on cases related to the financial crisis;

- Continued application of the Sarbanes-Oxley “clawback” remedy;

- Continued focus on insider trading, particularly by persons employed by hedge funds; and

- A warning to defense counsel to avoid conduct that is “questionable, or worse” in defending clients in SEC investigations.

A. The SEC Approves Final Rules To Implement The Dodd-Frank Whistleblower Provision

In May 2011, by a vote of 3-2, the SEC adopted final rules (“Whistleblower Rules”) to implement the whistleblower bounty program mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act. The Whistleblower Rules establish the standards and procedures the SEC will apply in awarding whistleblowers monetary compensation for providing tips about possible securities law violations that lead to successful SEC enforcement actions and define the contours for protections of whistleblowers under the Dodd-Frank Act’s anti-retaliation provisions.[3]

Eligibility for an award under the Whistleblower Rules generally can be summarized as follows: (i) a whistleblower, (ii) who voluntarily provides the SEC, (iii) with original information, (iv) that leads to a successful enforcement by the SEC that results in monetary sanctions of more than $1 million arising out of the same core facts, (v) is eligible for an award of 10 to 30 percent of any amounts recovered.

The Whistleblower Rules supplement the Commission’s ongoing efforts, along with its cooperation initiative, to incentivize individuals to report potential securities law violations to the SEC. In this respect, perhaps the most controversial aspect of the whistleblower rules is the extent to which the financial incentives threaten to undermine corporate compliance programs by leading employees to bypass internal reporting mechanisms in favor of reporting to the SEC in the first instance. The rules as adopted do not require an employee to report a complaint to the company first in order to be eligible for a reward. Rather, the rules provide that the amount of the reward may be higher if the employee reports the complaint internally and permit the employee complaint to the SEC to relate back up to ninety days to the date of the report to the company.

Ultimately, the Commission’s Whistleblower Rules present a challenge to all companies and regulated entities. The financial incentive to blow the whistle to the government will strain the most effective internal compliance programs. It will be more important than ever that companies’ compliance programs provide effective means for employees to report concerns internally, respond to complaints with a diligent, yet cost-effective, internal inquiry, and document the process and results for review if, and when, the SEC comes to conduct its own investigation. For a more in depth discussion of the Whistleblower Rules, see Gibson Dunn’s prior alert, “U.S. SEC Adopts Final Rules Implementing Whistleblower Provisions of Dodd-Frank.”

B. The SEC Announces Its First-Ever Deferred Prosecution Agreement

As part of its cooperation initiative unveiled in January 2010, the Enforcement Division announced a continuum of so-called cooperation tools, from proffer and cooperation agreements to deferred prosecution agreements (“DPA”) and non-prosecution agreements (“NPA”) to criminal immunity requests, designed to reward and incentivize cooperation by individuals.[4] One of the challenges we have noted that the SEC faces in motivating individuals to cooperate is that, unlike in the realm of criminal prosecutions, there is no developed public record demonstrating the rewards an individual would receive by cooperating.

Thus far, the Staff has stated on various occasions that they have entered into cooperation agreements with up to 25 individuals. However, as we predicted, to date, there has been no public record identifying an individual as a cooperator or the credit that individual received in return for their cooperation. As a result, experience for individuals with the cooperation initiative remains anecdotal.

Nevertheless, the SEC has made public use of two of its new cooperation tools — NPAs and DPAs — in cases involving corporations.

As we discussed in our last year-end alert, in December 2010, the SEC entered into an NPA with Carter’s Inc.[5] In May of this year, the SEC announced its first DPA, Tenaris S.A., to resolve alleged violations of the Foreign Corrupt Practices Act (“FCPA”).[6]

Pursuant to the DPA, Tenaris agreed to pay $5.4 million in disgorgement and interest relating to claims that it improperly procured Uzbekistani oil and gas contracts. Separately, Tenaris resolved a parallel investigation by the U.S. Department of Justice (“DOJ”) by entering into a separate NPA and agreeing to pay $3.5 million in fines. In announcing the DPA, Mr. Khuzami noted Tenaris’s “high levels of corporate accountability and cooperation,” including its “immediate self-reporting, thorough internal investigation, full cooperation with SEC Staff, enhanced anti-corruption procedures, and enhanced training made it an appropriate candidate for the Enforcement Division’s first Deferred Prosecution Agreement.”[7]

There are at least two notable distinctions between the DPA in Tenaris and the NPA in Carter’s. First, the DPA included an undertaking by the company to pay disgorgement. (This is not a necessary distinction between an NPA and a DPA, as an NPA could similarly include an undertaking to pay disgorgement.)

Second, and more important, the NPA made no allegations of misconduct and contained no factual recitation. In contrast, the DPA contained a detailed “Statement of Facts” similar to the allegations that would have appeared in a complaint to a settled injunctive action.[8] Moreover, under the terms of the DPA, in the event of a breach of the agreement and a subsequent enforcement action by the SEC, Tenaris agreed that it could not contest the facts as admissions. Thus, a DPA carries significant consequences for the company if violated and pursued by the SEC.

In addition, there is potential risk of collateral consequences to an agreement to an adverse statement of facts. Generally, courts have concluded that they will not impose collateral estoppel based on factual recitations contained in settled SEC enforcement actions and that settled SEC complaints or administrative orders are not evidence. Because DPAs are new, there is less precedent on how courts will view similar factual recitations. Beyond their effect in courts, DPAs may carry other collateral effects, such as suspension or disbarment of companies that obtain government contracts in the U.S. or Europe, or companies that perform projects with funds from international development banks (e.g., the World Bank). Such decisions are discretionary based on facts and circumstances, but the untested nature of the DPA carries some risk. For example, under the Federal Acquisition Regulation, a U.S. government agency may have the discretion to suspend a company “on the basis of adequate evidence” and disbar a company “based upon a preponderance of the evidence.”[9] Companies considering a DPA resolution will need to consider how the agreement and its statement of facts could affect these contractual relationships.

In recent remarks, Mr. Khuzami suggested that the Staff’s position on the appropriateness of a DPA versus an NPA may turn on the weight of the evidence of an underlying violation. Accordingly, a case of a clear violation, even with cooperation, could result in a DPA, while a case where a violation is less clear, but accompanied by cooperation, could result in an NPA.[10]

While DPAs and NPAs now appear to be alternative methods for a company to resolve an enforcement investigation, they remain an elusive disposition for individuals. Moreover, the detailed statement of facts that a DPA recites and to which a party must agree is a significant and potentially insurmountable disincentive to individuals to cooperate in an investigation if it involves conceding their own misconduct.

C. Statistics and Trends

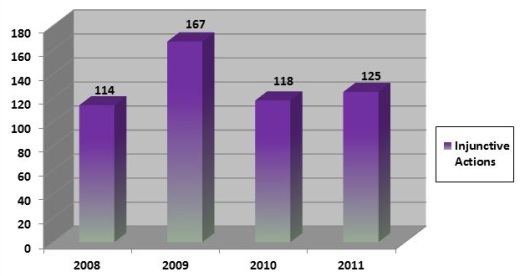

For the last four years we have been tracking certain metrics of enforcement activity and have identified noteworthy trends that have emerged. First, during the first six months of 2011, the SEC filed 125 civil injunctive actions in federal court. This is around the same number filed in the same period in 2010, when the SEC filed 118 civil actions, and in 2008, when the SEC filed 114 actions. However, this figure is down significantly from the peak number of actions the SEC filed in 2009.

Figure 1 – January to June Injunctive Actions Filed

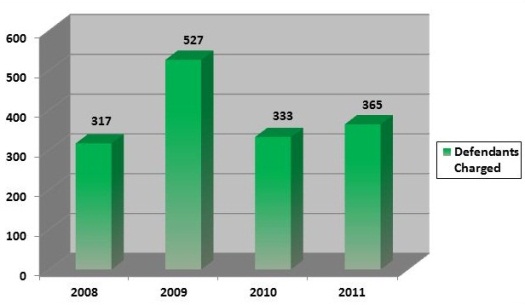

Similarly, in looking at the number of defendants charged, in the first six months of 2011, the SEC charged 365; which, similar to the number of injunctive actions filed, is largely in line with 2010 and 2008, when the SEC charged 333 and 347 defendants, respectively. This figure is down significantly from the peak of 527 defendants charged during the same period in 2009.

Figure 2 – January to June Number of Defendants Charged

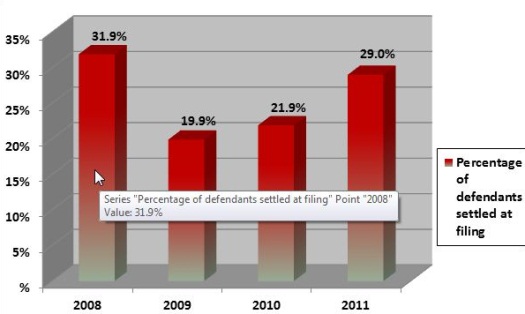

Last year, we noted a two-year trend of actions filed without settlement, suggesting the SEC’s willingness to litigate cases when it could not achieve the results sought in settlement. In 2011, we are beginning to see a slight break in this trend. In the first six months of 2011, 29% of defendants’ charged were settled at the time of filing. This is up from 2010 when 21% and from 2009 when 19% of defendants’ charges were settled at the time of filing. The 2011 figure suggests a return to the percentage in 2008 of 31%.

Figure 3 – January to June Percentage of Defendants Settled at Filing

D. Significant Cases

Since becoming Division Director, Mr. Khuzami has often stated that he seeks to measure the performance of the Division less through traditional quantitative metrics and more through qualitative measures, such as the programmatic importance of enforcement actions. Thus, the SEC has focused resources on investigating, filing and ultimately litigating, significant cases against financial institutions and senior executives, particularly in areas related to insider trading, director conduct and accounting fraud. We highlight certain significant cases below and discuss them in more detail in subsequent sections of this Review. The Commission has also continued its aggressive enforcement of cases of alleged illegal payments to foreign government officials under the Foreign Corrupt Practices Act. Those are discussed in Gibson Dunn’s 2011 Mid-Year FCPA Update.

1. Financial Crisis

The first half of 2011 saw the Commission continue to pursue actions in connection with the financial crisis. When asked recently to forecast how close the Staff is to the end of financial crisis related cases, Mr. Khuzami was non-committal: “We are in the fifth or sixth inning, but I don’t know if this is a single game or a double-header.”

In June 2011, two financial institutions reached settlements with the SEC in relation to allegations arising out of the financial crisis. First, J.P. Morgan Securities LLC settled claims that in selling a synthetic collateralized debt obligation (“CDO”), it did not adequately disclose that a portion of the assets in the CDO portfolio were selected by a hedge fund that held a short position in those assets.[11]

More significant, in an unsettled action, the SEC charged Edward Steffelin, a managing director at the investment advisory firm that served as collateral manager for the CDO, for allegedly failing to disclose in marketing materials the hedge fund’s role in selection of the collateral. What is significant is that the SEC charged the case under statutory provisions for which negligence alone (rather than intentional or even reckless conduct) could constitute a violation. The SEC’s pursuit of an individual under a negligence theory indicates the lengths to which the SEC is going to respond to calls to hold individuals accountable in the wake of the financial crisis.

Second, Morgan Keegan & Company and Morgan Asset Management settled previously filed allegations of failing to employ reasonable pricing procedures and failing to calculate accurate “net asset values” for five funds that Morgan Asset Management managed from January through July of 2007.[12] The firm’s former portfolio manager and comptroller also reached settlements with the SEC.

2. Insider trading

The SEC continued to focus emphasis on insider trading and hedge funds. In the last 18 months, 49 defendants have been charged in connection with insider trading by hedge funds. Of those, 46 have either pleaded guilty or been found guilty after trial. During the last six months, this trend continued with new charges stemming from the widespread investigation of trading linked to the Galleon Group and guilty verdicts against several defendants following trials. Among the significant developments are:

- Trial and guilty verdict against Mr. Rajaratnam on all 14 counts of securities fraud and conspiracy. Rajaratnam is scheduled to be sentenced on July 29.

- Trial and guilty verdict against Winifred Jiau, based on allegations that she obtained inside information from technology companies and then provided the information to hedge fund managers for a significant profit.

- Trial and guilty verdicts against Zvi and Emanuel Goffer and Michael Kimelman for insider trading based on tips received from an attorney concerning deals in which his firm’s clients were involved.[13]

- Insider trading charges against business consultant Rajat Gupta alleging that he tipped Raj Rajaratnam with inside information about the quarterly earnings at both Procter & Gamble and Goldman Sachs.[14] This case is also significant because it represents the SEC’s first use of an administrative proceeding to charge insider trading and to seek penalties under Dodd-Frank.

- Charges against six consultants connected to the expert consulting network Primary Global Research alleging that the consultants disclosed inside information concerning their public companies employers, to hedge funds in return for consulting fees.[15]

- Charges against hedge fund manager Joseph Skowron alleging trading in health care-related stocks after receiving tips from a medical researcher overseeing a drug trial that the results would be unsuccessful.[16] In settling the SEC’s claims, the FrontPoint-affiliated hedge funds agreed to pay back $33 million in disgorgement and interest without admitting any wrongdoing.[17]

The most significant procedural development to come out of the Galleon-related cases to date is the courts’ vindication of the use of wiretaps in insider trading investigations. In many of these cases, wiretaps have played a critical role in enabling the government to build cases that would otherwise have been difficult, if not impossible, to make. As a result, the government comes away from these cases encouraged in the continued use of wiretaps as a legitimate and effective tool for investigating insider trading, particularly against institutional traders.

3. Actions Against Independent Directors

SEC enforcement actions against independent directors of public companies are rare, which makes them all the more notable when brought.

In February 2011, the Commission charged three former independent directors and members of the audit committee of DHB Industries, Inc. (“DHB”).[18] The complaint alleged that the defendants facilitated DHB’s securities violations by turning “a blind eye to numerous, significant, and compounding red flags” signaling fraud and allowed senior management to file materially false and misleading filings with the Commission and use corporate funds to pay for personal expenses. For more information on this case, see our prior client alert, SEC Targets Directors Who Ignore Red Flags.

While cases against directors, acting solely in their capacity as directors, are infrequent, the Staff will inevitably investigate the knowledge and conduct of directors in any case which touches the boardroom. Cases such as this are a reminder of the importance of directors being able to demonstrate their diligence when confronted with red flags of potential misconduct by management.

4. Accounting Fraud — Clawback of Executive Compensation

The SEC continues to use section 304 of the Sarbanes-Oxley Act (“SOX”) to retrieve ill-gotten gains from CEOs and CFOs in 2011, even in the absence of allegations of misconduct by the executive. In March, the CEO of Beazer Homes, Ian McCarthy, as part of a settlement, agreed to pay back $6.5 million of compensation pursuant to section 304.[19] The SEC did not allege that McCarthy had engaged in any misconduct, but it had previously charged the company and its chief accounting officer with securities laws violations. Nevertheless, the SEC alleged that McCarthy failed to reimburse Beazer Homes for cash bonuses, incentive and equity-based compensation and profits from his sale of Beazer stock received during the 12-month period following the issuance of Beazer’s fraudulent quarterly and annual financial statements for its fiscal year 2006.[20]

With this type of case, it is clear that the SEC will continue to push this remedy against CEOs and CFOs who, despite the absence of misconduct on their part, are at the helm of a company during a financial reporting period that is subsequently restated due to the misconduct of others at the company.

5. Attorney Misconduct In SEC Enforcement Actions

During a speech on June 1, 2011, Director Khuzami took the opportunity to caution attorneys against engaging in overzealous defense tactics in SEC Enforcement investigations.[21] In the speech, Director Khuzami observed what he believed to be increasing incidences of questionable defense counsel behavior, including multiple representations of witnesses with adverse interests, witnesses who adopt implausible explanations of events or implausibly fail to recall certain events, signaling to clients during testimony and employment of questionable tactics in document productions and internal investigations. Director Khuzami warned that the SEC “can and will” utilize available tools to discourage such tactics, including referring obstructionist conduct to the SEC Office of General Counsel, referring obstructionist witnesses to the Department of Justice and examining evidence in light of the level of cooperation that the Commission receives. Recent proceedings suggest that the SEC is fully prepared to take action against defense attorneys when it believes their professional conduct to be inappropriate.

In January 2011, the Commission instituted administrative proceedings against an attorney for allegedly engaging in the type of improper professional conduct that Director Khuzami criticized in his speech on June 1. The SEC alleged that during an SEC examination of a broker-dealer in 2009, an attorney for the broker-dealer altered private placement memoranda (PPMs) used in a securities offering, before producing the PPMs to the Staff. The attorney allegedly added language to make it appear that the PPMs had disclosed that much of the money raised would be loaned to the broker-dealer’s principal.[22]

Cases against counsel based on conduct during an investigation or examination are rare. However, defense counsel (and clients) should understand that even simply an investigation by the SEC’s Office of the General Counsel of attorney conduct threatens to undermine counsel’s ability to continue representing the client, and thus the client’s choice of counsel. A more aggressive use of this power by the Commission could pose significant risks for counsel and clients alike.

E. What to Look for in the Second Half of 2011

The SEC’s focus on insider trading will continue and thus we expect to see additional cases being filed in this area. In addition, previously filed cases in this area will work their way through litigation and approach trial or result in settlements.

Now that the Whistleblower Rules have been approved, we also expect that there will be increased whistleblower activity over the coming months and years. Interestingly, during the June 1, speech referenced above, Director Khuzami took the opportunity to warn attorneys that overzealous defense tactics in the context of an SEC Enforcement proceeding may leave them vulnerable to a whistleblower claim, further emphasizing the far-reaching breadth of this new legislation.

Finally, the SEC appears to have turned its focus to the analysis of new trading technologies such as high frequency and algorithmic trading, data feed latency issues and large volume trading. In connection with this new area of emphasis, Director Khuzami observed that there are significant challenges stemming from the “fast-paced change and increasing complexity apparent in the financial products, markets, transactions, and practices the Division [of Enforcement] confronts.” Khuzami went on to note that the volume of information that the Commission receives each month is staggering, and has created a significant need for the Commission to develop more efficient processing and analysis methodologies.

II. Insider Trading

Insider trading enforcement has remained extraordinarily active in the last six months. The SEC has continued to pursue insider trading actions against hedge funds and expert networks, in addition to the traditional insider trading cases involving tipping and trading by corporate employees. The major developments are set out below.

A. Criminal Prosecutions

The government has won major criminal convictions against insider trading defendants in the past half year. In particular, the criminal prosecution against individuals connected to Galleon Management has resulted in several guilty pleas and verdicts. A jury found Galleon founder Raj Rajaratnam guilty of the fourteen conspiracy and securities fraud charges brought.[23] Zvi Goffer, a former employee of Galleon, was found guilty of insider trading through acquiring tips from attorneys at corporate law firms.[24] Goffer’s brother Emanuel and Michael Kimelman were also found guilty of conspiracy and securities fraud.[25] Winifred Jiau, a former-expert network consultant, was also found guilty in June 2011 of passing insider information she gained from consultants.

1. SEC v. Galleon Management and Related Cases

The use of wiretaps has been one of the distinguishing features of the Galleon and related investigations. Wiretaps present unique issues in parallel criminal and civil investigations because criminal investigators and prosecutors are restrained from sharing the results of wiretaps with the SEC. Nevertheless, subsequent litigation in the SEC’s civil case against Rajaratnam demonstrated that the SEC may still obtain the results of wiretaps from the defendant through civil discovery. [26] Last year, the Second Circuit held that a district court may order production to the SEC of wiretap evidence obtained by a defendant in discovery in a parallel criminal proceeding but that production is not universally permitted. In deciding whether production is appropriate, a district court must balance the SEC’s interest in obtaining discovery against the defendants’ privacy interest. The Court of Appeals held that the district court exceeded its discretion by issuing the discovery order. In May of this year, on remand, the district court held that the SEC’s interest in obtaining discovery outweighed the defendants’ privacy interests and issued another order for the production of the wiretaps.[27]

Since the beginning of 2011, the SEC has brought three more complaints against individuals in hedge funds, investor consulting firms and law firms related to the Galleon investigation.[28] Further, five individuals in the Galleon cases agreed to settle charges in 2011.[29] Vice President of Broadband Carrier Networking at Atheros Communications, Inc. Ali Hariri settled charges that he provided insider information to a co-defendant. Robert Moffatt, a Senior Vice President and Group Executive of IBM, agreed to settle charges that he tipped material nonpublic information which allowed a co-defendant and Mark Kurland to profit from this information. Mark Kurland, CEO of New Castle Funds, LLC, similarly settled charges that he traded on material nonpublic information. Adam Smith, a portfolio manager at Galleon Management, also settled charges that he traded on insider information obtained from various sources. Shammara Hussain, an employee at Market Street Partners, settled charges that she provided nonpublic information about Google to traders at Galleon.

B. Administrative Proceedings

The Dodd-Frank Act extended the SEC’s authority to impose monetary penalties beyond SEC-registered entities and associated persons, to any person or entity. In a recent insider trading case, the SEC has tried to use this authority, and as a result, has been met with a constitutional challenge in federal court. In March 2011, the SEC brought an administrative cease-and-desist proceeding against Rajat Gupta, formerly a director of Goldman Sachs and Proctor & Gamble, alleging that he disclosed material nonpublic information to Raj Rajaratnam regarding Berkshire Hathaway’s impending $5 billion investment in Goldman Sachs and other nonpublic financial results of Goldman Sachs and Proctor & Gamble.

An administrative proceeding is generally viewed as a more favorable venue for the Enforcement Division because it affords the respondent no discovery, other than access to the staff’s investigative file, and ensures a bench trial before the SEC’s administrative law judges rather than a jury in an Article III court, and an appeal to the Commission. As such, administrative proceedings where the Enforcement Division will seek civil monetary damages are likely to become much more common as the staff seeks to litigate these cases in a more advantageous forum.

In response, Gupta denied the charges and filed a complaint in federal court against the SEC. Gupta is challenging the legality of the administrative proceedings filed against him, including the retroactive application of the Dodd-Frank Act — the alleged insider trading occurred 1½ years before enactment of the Dodd-Frank Act. Gupta has also challenged the due process constitutionality of the administrative proceeding, alleging that the proceeding’s more lenient procedure, evidentiary standards and deference afforded to any award from any appellate review would deprive Gupta of his constitutional rights. On July 11, the Court presiding over Gupta’s suit ruled that he could proceed with his equal protection claim against the Commission.[30] This ruling comes on the heels of an order in the administrative proceeding postponing the proceeding for six months at the request of the parties.[31]

C. Expert Networks

In 2011 the SEC has continued to focus on the expert networks industry. In February 2011, the SEC filed a civil suit against two employees of “expert network” Primary Global Research, four technology employees and four defendants from hedge funds for insider trading.[32] The complaint alleges that the technology employees, who also worked as Primary Global consultants, disclosed material nonpublic information about sales, earnings or performance data at various public technology companies to Primary Global’s hedge fund clients for compensation, which resulted in nearly $6 million in alleged profits.[33] In the parallel criminal proceedings, one of the consultants who contested the charges, Winifred Jiau, was found guilty after a trial. Another defendant, James Fleishman, a former employee of Primary Global, is scheduled for trial in August. Another former Primary Global executive, Don Chu, pled guilty in June.[34]

These cases demonstrate the unique risks created by the use of expert networks. It is essential that advisers that permit the use of expert networks have in place comprehensive policies and procedures to mitigate those risks. These may include procedures at the front end to vet the use of particular networks, as well as sample back testing of trades in securities discussed with expert consultants.

D. M&A Insider Trading

In the first half of 2011, the SEC has brought several insider trading charges for trading in advance of merger announcements. In January, the SEC filed a complaint against George Holley, the former chairman of Home Diagnostics Inc., alleging that he tipped friends about the upcoming acquisition of the company and provided funds to two of them to purchase Home Diagnostics stock.[35]

The SEC also filed a complaint against Zhenyu Ni for insider trading of Bare Escentuals, Inc. securities.[36] The SEC alleged that, while visiting the office of his sister, a Bare Escentuals executive, Ni overheard a conversation revealing the unannounced acquisition of Bare. Ni purchased Bare stock and earned profits of $175,066. The SEC alleges that Ni misappropriated the information from his sister.

The SEC also settled or resolved several cases in the first half of 2011. The SEC recently resolved its previously filed case against Mitchell Sacks and Alfred Teo for insider trading C-Cube shares.[37] The SEC alleged that Teo, director of a potential acquirer of C-Cube, tipped Sacks on the acquisition. Sacks settled the charges[38] while Teo was found liable for securities fraud and disclosure violations.[39] Lorenz Kohler also settled charges with the SEC, on charges that he used nonpublic knowledge of a merger between CNS Inc. and GlaxoSmithKline to realize profits of $387,566.[40]

E. Insider Tips from Drug Trials

The SEC continued its investigation of the insider trading charges of Dr. Yves Benhamou by bringing charges against Dr. Joseph Skowron, a former portfolio manager for six health care-related hedge funds affiliated with FrontPoint Partners.[41] The SEC brought its original charges in November 2010 and amended its complaint in April 2011. Dr. Benhamou is accused of tipping Skowron with nonpublic material information concerning negative results of a clinical drug trial.

The SEC has also brought charges against Cheng Yi Liang, a chemist at the Food and Drug Administration, alleging that Liang traded in advance of at least 27 public announcements about FDA drug approval decisions involving 20 publicly traded companies and profited by more than $3.6 million.[42]

F. Attorneys

In the first half of 2011, the SEC has brought several charges or continued their cases against several attorneys for insider trading. In April 2011, the SEC charged Matthew Kluger, a corporate attorney, and Garrett Bauer, a self-employed broker-dealer, with insider trading in advance of at least 11 merger and acquisition announcements involving clients of Kluger’s law firm.[43] Parallel criminal charges were also brought against Kluger and Bauer. The SEC charges that Kluger accessed his law firm employer’s internal document management system to find nonpublic material information concerning the mergers and acquisitions of the law firm’s clients. Bauer then placed trades on the confidential information for himself and Kluger. The SEC alleges that Kluger and Bauer illegally profited at least $500,000 and $32 million, respectively. A third individual, Kenneth Robinson, who was the middleman between Kluger and Bauer, cooperated in the investigation, and entered into a plea agreement in the parallel criminal case.[44]

In March 2011, the SEC charged Todd Treadway, a corporate attorney, with insider trading.[45] The SEC alleges that Treadway used information he obtained while advising clients on the employee benefit and executive compensation consequences of mergers and acquisitions to purchase stock in two separate companies before their announcement of the acquisitions.

The government continued to advance cases against defendants who traded on tips from corporate attorney Arthur Cutillo about clients of his law firm. In the criminal case, defendants Zvi and Emanuel Goffer and Michael Kimelman were found guilty after trial. In June, the SEC settled its case with Gautham Shankar.[46] The SEC alleged that Shankar, while working as a propriety trader at the broker-dealer Schottenfeld Group, LLC, used inside information tipped from Zvi Goffer to place trades before the announced acquisitions of Avaya Inc. and 3Com Corp. The SEC also alleged that Shankar passed this insider information on to a friend.

III. INVESTMENT ADVISERS

A. Implementing Dodd-Frank: Rulemaking and Related Studies

1. New Rules Adopted by the SEC

As part of its implementation of the Dodd-Frank Act, on June 22, the SEC adopted several important rules for investment advisers:[47]

Reporting Requirements for Hedge Funds and Other Investment Advisers. To enhance its ability to oversee investment advisers to private funds, the Commission is requiring those advisers to provide additional information on their registration forms about the private funds they manage. Such advisers will now have to provide basic organizational and operations information about each fund they manage, and identify five categories of “gatekeepers”–auditors, prime brokers, custodians, administrators, and marketers. The Commission is also adopting amendments to the adviser registration form which require all registered advisers to provide more information about their advisory business, including information about the types of clients they advise, their employees, their advisory activities and their business practices that may present significant conflicts of interest.

Reporting Requirements for Exempt Advisers. Exempt reporting advisers will now be required to file, and periodically update, reports with the Commission. While exempt advisers are required to use the same registration form as registered advisers, they need only fill out a limited subset of the items on that form, including basic identifying information, and information about conflicts of interest and the adviser’s disciplinary history.

Reallocation of Regulatory Responsibility. Since 1996, regulatory responsibility for investment advisers has been divided between the Commission and the states, primarily based on the amount of money an adviser manages for its clients. The Dodd-Frank Act raised the threshold for Commission registration from $25 million to $100 million by creating a new category of advisers called “mid-sized advisers”–advisers that have assets under management of between $25 million and $100 million–that are subject to state registration. The Commission is adopting amendments to several of its current rules and forms to: reflect the higher threshold for Commission registration; provide a buffer to prevent advisers from having to frequently switch between Commission and state registration; clarify when an adviser is a mid-sized adviser; and facilitate the transition of advisers between federal and state registration in accordance with the new requirements.

Pay-to-Play. The Commission is amending the investment adviser “pay-to-play” rule in response to changes made by the Dodd-Frank Act. Under the amendment, an adviser will be permitted to pay a registered municipal adviser to act as a placement agent to solicit government entities on its behalf, if the municipal adviser is subject to a pay-to-play rule adopted by the Municipal Securities Rulemaking Board that is at least as stringent as the investment adviser pay-to-play rule. Advisers will continue to be permitted to hire as a placement agent an SEC registered investment adviser or a broker-dealer that is subject to a pay-to-play rule adopted by FINRA that is at least as stringent as the investment adviser pay-to-play rule.

Exemptions for Certain Advisers. The Dodd-Frank Act eliminated the private adviser exemption and created three new exemptions for: advisers solely to venture capital funds; advisers solely to private funds with less than $150 million in assets under management in the United States; and certain foreign advisers with a place of business in the United States. The Commission is adopting rules that would implement these exemptions and define various terms.

2. Studies Published by the SEC

In addition to these new rules, the SEC released three studies mandated by Sections 913, 914, and 919B of the Dodd-Frank Act, which relate to improving the investment adviser and broker-dealer regulatory frameworks.[48] All three studies were published in January.

Investor Access to Registration Information.[49] Currently, investors interested in retaining investment advisers must consult two separate repositories for registration information–the Central Registration Depository (for broker-dealers) and the Investment Adviser Registration Depository (for investment advisers). Each database in turn has different search capabilities and delivery systems for distilling and transmitting information to users. This balkanized approach to storing and delivering registration information increases the burdens on investors and may enable substandard advisers to continue to retain new business.

In response to Section 919B of the Dodd-Frank Act, which required the Commission to study potential improvements in this area, the Staff’s study concluded that there would be significant advantages to centralizing the two registration systems, though full integration of each database could not be completed within Section 919B’s timeframe for implementation. As a result, the study recommended unifying each system’s search results, instituting additional searching capabilities (to include zip code and other locations functions), and annotating search results with educational content to make the delivered registration data more approachable to unsophisticated investors.

Fiduciary Duty of Investment Advisers and Broker-Dealers.[50] The financial crisis has resulted in increased scrutiny of investment advisers and their disclosure obligations. In response, Section 913 of the Dodd-Frank Act instructed the Commission to explore: (1) the effectiveness of existing legal or regulatory standards of care that apply when broker-dealers and investment advisers are providing personalized investment advice and recommendations about securities to retail customers; and (2) whether there are any legal or regulatory gaps, shortcomings or overlaps in these legal or regulatory standards that should be addressed by rule or statute.[51] This report is discussed in more detail in the next section on broker dealers.

Investment Adviser Examinations.[52] The SEC’s system of investment adviser examinations has come under increasing strain in recent years as the number of registered investment advisers has grown considerably at the same time that the Staff of the SEC’s Office of Compliance Inspections and Examinations (“OCIE”) has steadily decreased. Between 2004 and 2010, the OCIE’s Staff dedicated to examinations decreased by 3.6% while the number of registered investment advisers grew by 38.5%. As a result, the OCIE Staff managed to examine only 9% of all registered investment advisers in 2010, down from 18% in 2004.

To ensure resources adequate to meet expected future workload, the Staff’s study, undertaken in response to Section 914 of the Dodd-Frank Act, recommended that Congress consider the following three approaches to strengthen the examination regime:

- User Fees: One alternative considered by the study was that user fees collected from investment advisers would be earmarked to provide stable financing for the OCIE’s examination efforts. Because the OCIE’s Staff would remain in place, this approach would have the added benefits of maintaining the SEC’s institutional competency in this area while avoiding the inefficiencies and supervisory obligations associated with delegation of responsibility to one or more Self-Regulatory Organizations (“SROs”). As such, the study appears to favor this option over the other two alternatives.

- SROs: The study also explored the use of one or more SROs to augment the OCIE’s examination program. As the study notes, experience indicates that joint efforts with the industry can in fact enhance regulatory efforts, but many issues would have to be addressed to create a working SRO system, including the number of SROs, as well as their authority, membership, governance and funding. Further, the OCIE would be required to retain supervisory authority, and, with that would come the need for funding and oversight staffing.

- FINRA: The final alternative considered, which the study admitted was less comprehensive than the user fee or SRO options, was to task FINRA with examining “dual registrants,” namely advisers registered under the Investment Advisers Act of 1940 that are also registered broker-dealers. This approach would avoid many of the general drawbacks seen in a SRO-based examination system. But the examination coverage would be incomplete, and this solution would run the risk of divergent or even conflicting findings between FINRA and the OCIE.

B. Investment Adviser Cases

1. Mortgage-Backed Securities

In January, the SEC instituted a settled action against Charles Schwab Investment Management (“CSIM”) and Charles Schwab & Co., Inc. (“CS&Co.”) relating to the Schwab YieldPlus Fund, formerly the largest ultra-short bond fund in its class, but whose assets fell from $13.5 billion to $1.8 billion between 2007 and 2008. The SEC alleged that the respondents misstated the risks of the fund and the extent of redemptions the fund was experiencing.[53] The SEC also alleged that certain fund of funds and fund managers, aware of the fund’s risks redeemed their investments, and therefore the SEC alleged that the respondents lacked adequate policies and procedures to prevent the misuse of material, non-public information. The respondents also allegedly deviated from the fund’s 25% concentration policy regarding investment in private-issuer mortgage-backed securities without obtaining requisite shareholder approval. Without admitting or denying the allegations, the respondents agreed to pay more than $118 million in settlement. The SEC also filed unsettled actions against two former Schwab executives.

In June, Morgan Keegan & Company and Morgan Asset Management agreed to pay $200 million to settle previously filed actions by the SEC, state regulators, and FINRA related to the valuation of subprime mortgage-backed securities.[54] Two Morgan Keegan employees also agreed to settlements that include penalties and, for one, an industry bar. The case alleged a failure to perform pricing procedures of subprime mortgage-backed securities in five funds managed by Morgan Asset Management, and consequently a failure to calculate accurate “net asset values” for the funds.

2. Insider Trading

In April, following a hearing, an SEC Administrative Law Judge issued an initial decision (which became final in May), finding that David W. Baldt, portfolio manager for municipal bond funds at Schroder Investment Management North America Inc. (“Schroder”), engaged in insider trading by tipping family members to redeem shares in funds he managed.[55] According to the decision, as of September 2008, portfolio managers at Schroder, including Baldt, were concerned about the financial state of various funds under their management, in particular after investor redemptions began to increase and the funds encountered difficulty in liquidating assets. Several of Baldt’s family members allegedly redeemed their holdings in various funds after learning material, non-public information from Baldt on the health of the Schroder funds. The decision ordered disgorgement of losses avoided by his family members through their redemptions and barred Baldt from association with an investment adviser, but the ALJ declined to impose a civil penalty finding it was not in the public interest.

3. Fees

In January, the SEC instituted settled administrative proceedings against two individuals, former co-portfolio managers of the Tax Free Fund for Utah (“TFFU”), who, while working for Aquila Investment Management LLC (“Aquila”), allegedly charged municipal bond issuers a one-time “credit monitoring fee” on certain non-rated and private placement bonds in TFFU’s portfolio. According to the order, any credit monitoring work the respondents performed would have been part of their regular job responsibilities. The respondents allegedly did not disclose the fees to Aquila or TFFU.[56] In settling the charges, the respondents agreed to disgorgement of the fees, penalties and industry bars.

In June, the SEC instituted settled administrative proceedings against Pegasus Investment Management, LLC (“PIM”) and several of its principals for violation of duties to fund investors, stemming from PIM’s alleged receipt of undisclosed cash payments in connection with its trading activities.[57] These payments were allegedly received from a proprietary trading firm in return for combining that firm’s trades with PIM’s trades, thus enabling the trading firm to obtain reduced commissions. The SEC alleged that PIM improperly treated the cash payments as its own assets rather than those of its fund investors. In settling the charges, PIM agreed to disgorgement of the allegedly improper fees totaling $90,000 plus prejudgment interest, and each PIM principal agreed to additional financial penalties.

4. Risk Management and Investor Disclosures

It is not often that the SEC brings an enforcement action against an investment adviser that follows a quantitative investment strategy. This year, the SEC brought an action that highlights one of the regulatory risks that quantitative funds face, namely the risk of errors in code that governs a particular investment strategy.

In February, the SEC instituted settled administrative proceedings against three AXA Rosenberg entities (“AXA”) arising from an error in the computer code of the quantitative investment model it used to manage client assets which disabled a component for managing investment risk.[58] The SEC alleged that a senior executive at AXA became aware of the error in the model’s code. Even though the error was fixed within four months, the SEC alleged that the executive’s failure to disclose the error constituted a material omission in violation of section 206 of the Advisers Act. In addition, the SEC alleged that the respondents failed to conduct sufficient quality control over the coding process and thus violated Rule 206(4)-7 by failing to have reasonable policies and procedures in place. In settlement, the respondents agreed to reimburse investors $217 million, pay a $25 million penalty and retain an independent consultant with expertise in quantitative investment techniques to review its disclosures and enhance the role of its compliance personnel.

Finally, in May, the SEC instituted settled administrative proceedings against Aletheia Research and Management, Inc. (“Aletheia”) and two of its principals, alleging that Aletheia did not properly address questions regarding the firm’s regulatory history in its responses to requests for proposals and other inquiries from prospective investors.[59] Specifically, the SEC alleged that Aletheia did not disclose accurate information about whether it had been subject to “findings,” “deficiencies” or “corrective actions” in connection with past SEC examinations. As part of the settlement, Aletheia agreed to pay $200,000 in penalties, and each principal agreed to pay $100,000; Aletheia also agreed to engage an independent compliance consultant to examine the firm’s compliance with the Investment Advisers Act.

IV. Broker/Dealers

A. SEC Regulatory Proposals and Recommendations

On January 21, 2011, the SEC Staff released its Study on Investment Advisers and Broker-Dealers, as required by Section 913 of the Dodd-Frank Wall Street Reform and Consumer Protection Act,[60] recommending rulemaking to establish a uniform fiduciary standard for broker-dealers and investment advisers who provide personalized investment advice to retail investors regarding securities. The recommended standard would supplement the regulatory framework in place and would be consistent with the standard under the Investment Advisers Act of 1940. It would also focus on the standard of care due investors, including acting in the best interest of the investor without regard to the financial interest of the broker-dealer or investment adviser.[61] The study explained that retail investors often do not grasp the differing roles played by broker-dealers and investment advisers, and therefore, uniform protection when receiving personalized advice would help alleviate some of this confusion.[62] Moreover, the study also suggested the possible harmonization of the broker-dealer and investment adviser regulatory regimes, particularly where broker-dealers and investment advisers perform substantially similar duties.[63] However, in a statement issued by SEC Commissioners Kathleen L. Casey and Troy A. Paredes, the Commissioners made clear that any rulemaking born out of the study’s recommendations alone would be deficient and potentially deleterious; they opposed the Study’s release to Congress in its current form without further research into investor demographics and preferences, in addition to more rigorous economic and data-based analysis.[64] The Commissioners’ primary critique centered on the Study’s alleged failure to adequately justify its recommendations, namely, whether its proposed regulation would in fact address the problems identified and at what cost.

On June 15, 2011, the SEC unanimously proposed amendments to the broker-dealer financial reporting rule, focusing on the custody activities of broker-dealers.[65] Much like the rules adopted by the SEC in December 2009 reinforcing the protections afforded investors who turn their assets over to investment advisers, the proposed amendments are aimed at strengthening the annual audits of broker-dealers and the SEC’s oversight of broker-dealer management of clients’ assets, including the controls in place.[66] Broker-dealers would be required to permit SEC Staff, and the designated examining self-regulatory organization, access to the working papers of their accounting firm auditors and permission to discuss any such findings with the accounting firm. Additionally, all broker-dealers would be required to file a proposed new form each quarter detailing information about their custody practices which would serve as an initial basis for examinations by regulators.

B. Compliance Related Cases

In recent months, chief compliance officers and the activities of their departments have become more frequent targets of SEC and FINRA enforcement actions, as enforcement officials have increased their scrutiny of the compliance procedures put in place by broker-dealers. The amplified interest in investor protection controls of broker-dealers has led to an uptick in compliance-related cases.

In January, the SEC brought a settled administrative action against Merrill Lynch for alleged improper use of customer order information.[67] The SEC alleged that the respondent failed to establish and maintain written policies and procedures designed to prevent the misuse of material nonpublic information as the firm’s proprietary trading desk obtained information about institutional customer orders from traders on the market making desk, and allegedly used the information in placing trades for Merrill subsequent to executing trades for the customers. The SEC also cited Merrill for charging its customers undisclosed mark-ups and mark-downs in filling customer orders at less favorable prices than those at which Merrill bought and sold the securities in the market. Without admitting or denying the SEC’s allegations, Merrill agreed to pay $10 million in settlement.

In February, the SEC brought a settled administrative action against TD Ameritrade for failing to reasonably supervise certain registered representatives who allegedly misstated to customers the risks and liquidity of the Reserve Yield Plus Fund.[68] A number of representatives allegedly characterized the fund as a safe money market fund with guaranteed liquidity when, in fact, it was a mutual fund that “broke the buck” in September 2008. The SEC alleged that the respondent failed to have adequate supervisory policies and procedures governing the offers and sales of the fund or to prevent the alleged misstatements from being made to investors. Without admitting or denying the allegations, TD Ameritrade agreed to distribute approximately $10 million to eligible customers still holding shares of the fund.

In April, Wells Fargo Securities LLC settled charges stemming from Wachovia Capital Markets LLC’s violation of investor protection rules under the securities laws in connection with two CDOs tied to the performance of residential mortgage-backed securities in late 2006 and early 2007.[69] Wachovia Capital Markets, since renamed Wells Fargo Securities, allegedly charged undisclosed and excessive mark-ups in its sale of preferred shares of a CDO, as the investors paid over 70 percent more than the price at which the equity was marked for accounting purposes. This was due to a compliance gap involving the failure to monitor mark-ups coming from the syndicate desk that originated the CDO. Moreover, in a second CDO, Wachovia Capital Markets allegedly misstated that it acquired securities at arms-length for fair market value when, in fact, they were transferred from an affiliate at above-market prices. Without admitting or denying the allegations, Wells Fargo Securities agreed to pay over $11 million in penalties and disgorgement.

Just a few days later in April, the SEC charged a former chief compliance officer, Mark A. Ellis, at Tampa-based GunnAllen Financial Inc., and two of its other executives in connection with the improper transfer of customer records during the winding down of GunnAllen.[70] The SEC alleged that information from over 16,000 GunnAllen accounts were transferred to the new employer of one of the executives without giving the customers reasonable notice to opt-out. Ellis, who agreed to a $15,000 penalty without admitting or denying the allegations, was cited for aiding and abetting the violations by failing to ensure that there were firm policies and procedures in place reasonably designed to safeguard confidential customer account information, especially following the theft of three company laptops. This was the first time the SEC assessed financial penalties against individuals based solely on the violation of Regulation S-P, a rule requiring financial firms to protect confidential customer information from unauthorized dissemination.

Finally, FINRA has also brought recent cases against compliance officers, suspending the former chief compliance officer of Meadowbrook Securities, LLC, Jay Lynn Thacker, for six months from acting in any principal capacity and fining Thacker $10,000 for failing, as the supervisory principal, to conduct a reasonable investigation in connection with the sale of private placements offered by Medical Capital Holdings, Inc. and Provident Royalties, LLC.[71] FINRA found that Meadowbrook had no reasonable grounds to believe the private placements were suitable investments for its customers given that it did not perform adequate due diligence in order to ascertain the risks inherent to the offerings in question. The broker-dealer was especially derelict because liquidity concerns, missed interest payments and defaults would have come to light had the proper diligence been done.

C. Sales Practices, Preferential Treatment and Fraud

In January, a New York-based broker, Paul George Chironis, settled charges brought against him in April 2010 in which the SEC found that he churned two charitable accounts by engaging in excessive trading to generate commissions without regard for the customer’s investment needs.[72] Chironis’ high turnover trading strategy led to undisclosed and excessive costs being incurred, including undisclosed mark-ups and mark-downs in riskless principal transactions. Over a 13-month period, the accounts paid approximately 10.8 percent of their value to Chironis in transaction fees. Without admitting or denying the allegations, Chironis agreed to pay $350,000 in disgorgement and penalties and an industry bar.

In March, the SEC charged former UBS Financial Services financial advisor, Steven T. Kobayashi, with misappropriating $3.3 million from a pooled private investment fund he created to invest in life insurance policies.[73] The SEC alleged that Kobayashi stole at least $1.4 million for his personal expenses and concealed the fraud by liquidating his other customers’ securities to replace the money in the fund, thereby stealing an additional $1.9 million. Without admitting or denying the allegations, Kobayashi agreed to be permanently barred from the securities industry; the Court will determine disgorgement and penalties at a later date.

Later in March, the SEC filed a civil injunctive action against, James J. Konaxis, a former registered representative of Massachusetts-based broker-dealer Sentinel Securities, Inc. for churning the account of a customer who invested the money she received from the September 11th Victim Compensation Fund.[74] Over a two-year period, the respondent allegedly received approximately $550,000 in commissions, while the value of the customer’s account fell from approximately $3.7 million to approximately $1.6 million. Konaxis agreed to partially settle the charges by consenting to an industry bar, with disgorgement and penalties to be determined at a later date.

Recently, on June 15th, the SEC found that customers who were sold certificates of deposit issued by Stanford International Bank Ltd. through the broker-dealer Stanford Group Company are entitled to protected “customer” status under the Securities Investor Protection Act of 1970 (SIPA) as a result of the Ponzi scheme conducted by Allen Stanford, the owner of the broker-dealer.[75] The SEC determined that there was no corporate separateness among the Stanford entities, as money flowed from one to another, all in support of the Ponzi scheme. The SEC has requested that the Securities Investor Protection Corporation (SIPC), of which the Stanford Group Company is a member, initiate a judicial proceeding under SIPA to liquidate the Stanford Group Company, allowing the wronged investors to file claims with a trustee selected by SIPC. Should SIPC not initiate such a proceeding, the SEC has authorized the staff to file a federal action under SIPA to compel SIPC to do so.

On June 24, 2011 the SEC set aside the FINRA decision fining American Funds Distributors $5 million for the allegedly improper direction of approximately $98 million in brokerage commissions to brokerage firms that were top sellers of American Funds from 2001 to 2003, thereby rewarding them for past sales and encouraging future sales.[76] While quid pro quo arrangements between broker-dealers and fund firms for the purpose of spurring fund sales are unlawful, American Funds claimed that it only had informal targets for directing trades, and that the sales were not the only consideration for the directed trading, a practice permitted under the NASD rules in place. In light of evidence relating to American Funds Distributors’ compliance efforts, and the uncertainty resulting from the language of Rule 2830(k)(3) in effect during the period at issue before the clarifying 2004 Amendments, the SEC set aside the NASD’s enforcement action since the defendant was not afforded “fair notice” that its practices were prohibited.

D. Financial Crisis

In March, Enforcement Division Director Robert Khuzami stated “it is no secret that a priority for us has been misconduct arising out of the financial crisis,” having filed 20 cases and suing 40 defendants, including 26 CEOs, CFOs and other senior officers in actions involving “core financial crisis conduct.”[77] Moreover, fifteen of those cases have been settled, in whole or in part, resulting in over $1.3 billion in disgorgement, penalties and other monetary damages.[78]

On June 21st, the SEC brought a settled action against J.P. Morgan arising from the structuring and marketing of a synthetic CDO in 2007.[79] The SEC alleged that, while the marketing materials indicated that the assets in the CDO would be selected by an independent manager, a hedge fund with a short position in a portion of the assets, helped select the assets underlying the portfolio. Without admitting or denying the allegations, J.P. Morgan agreed to pay $153.6 million in settlement and improve its review and approval of transactions in mortgage securities.

In 2009, the SEC filed an unsettled action against Morgan Keegan alleging misrepresentations concerning the liquidity of auction rate securities (“ARS”). Unlike other firms that settled similar allegations, Morgan Keegan contested the SEC’s case and recently prevailed. On June 28, the Northern District Court in Georgia granted Morgan Keegan’s motion for summary judgment and dismissed the SEC’s action, finding that the SEC failed to produce sufficient evidence that the defendant had a policy of misstating the risks of ARS.[80] The SEC had alleged that the firm advised customers that ARS were safe, highly liquid securities akin to money market funds even as the market for ARS was deteriorating. In support of its allegations, the SEC produced statements from four investors. The court found that the evidence from four investors was insufficient to demonstrate a firm-wide policy and thus did not provide grounds for class-wide relief. The court also found that “the failure to predict the market does not amount to securities fraud.”[81]

The day following the Morgan Keegan decision, on June 29, the SEC announced a settled action against Raymond James & Associates and Raymond James Financial Services for allegedly misstating the liquidity of ARS and failing to adequately disclosure the risks of ARS and their dependence on auctions for liquidity.[82] Without admitting or denying the allegations, Raymond James agreed to a settlement that includes repurchasing illiquid ARS from customers and paying the difference to customers who sold their ARS at below par values.

E. Market Manipulation

In February, the SEC charged three individuals and two firms, including broker-dealer Hunter World Markets Inc. (“HWM”), with manipulating multiple microcap stocks between September 2005 and September 2007, generating over $63 million through sales of stock, commissions, and sales credits.[83] By taking microcap companies public through reverse mergers, and manipulating the stock prices upward before selling shares at magnified prices, one of the co-conspirators succeeded in overstating his hedge funds’ performance by at least $440 million, a practice called “portfolio pumping.” Using a secret, alternative messaging system to conceal their communications, the perpetrators carried out their international scheme by placing matched orders, placing orders that set the closing price for the day, and conducting wash sales. HWM’s chief compliance officer agreed to a $20,000 penalty and a one-year suspension from being a supervisor with a broker or dealer. The SEC seeks permanent injunctive relief, penalties, disgorgement and prejudgment interest.

F. Municipal Securities

Among the specialized units created within the Division of Enforcement is one unit devoted to Municipal Securities and Public Pensions. In the last six months, that unit has brought three enforcement actions, in coordination with other federal and state agencies, alleging misconduct in the bidding process for municipal bond reinvestment transactions. The three actions were against Banc of America Securities in December 2010, UBS Financial Services in May 2011 and J.P. Morgan Securities in July 2011.[84]

In summary, each of these cases involves similar allegations. Municipalities may temporarily invest proceeds of municipal securities sales in reinvestment products. In order to preserve tax exempt status, the proceeds should be invested at fair market value, which is commonly established through a competitive bidding process by investment providers and their agents. In these cases, the SEC alleges that the defendants entered into agreements that undermined the competitive bidding and thus deprived certain municipalities of a conclusive presumption of fair market value and jeopardized the tax-exempt status of certain municipal securities. Collectively, the cases thus far have resulted in monetary settlements with federal and state regulators in excess of $500 million.

In addition, the SEC barred James Hertz, a former J.P. Morgan Securities vice president and marketer, from associating with any broker, dealer, investment adviser, or the like, and from participating in any penny stock offering. Hertz had pled guilty in December 2010 in connection with his involvement in the bidding process and cooperated in the regulatory investigations.

V. Public Company Accounting and Financial Reporting

A. An International Focus

Signaling an increased focus on accounting fraud at internationally-based companies, the SEC created a task force to investigate accounting fraud by non-U.S. companies that trade in public U.S. markets. In an April 27, 2011 letter to Congressman Patrick McHenry, Chairman Schapiro touted the Commission’s aggressive actions against foreign issuers based in the People’s Republic of China (“PRC”).[85] Chairman Schapiro noted that twenty-four China-based companies revealed auditor resignations or accounting problems to the Commission, and that the SEC revoked the registrations of eight Chinese companies due to accounting irregularities.

A striking–and widely reported–international accounting fraud was Satyam Computer Services Limited, based in India. In April, the SEC announced settled civil charges against Satyam for what the SEC alleged to be a massive accounting fraud that resulted in the fraudulent overstatement of Satyam’s revenues by $1 billion in a five-year period.[86] Former Satyam employees created thousands of fake invoices and even created phony bank statements reflecting supposed payments related to the fictitious invoices. Satyam’s outgoing Chairman compared maintaining the fraud to “riding a tiger, not knowing how to get off without being eaten.” Under new management appointed by the Indian government, Satyam agreed to settle the charges and paid a $10 million civil penalty.

Satyam’s independent auditors agreed to settle charges as well. Five India-based PricewaterhouseCoopers affiliates agreed to pay $6 million in penalties, the largest-ever amount in a Commission investigation against a foreign-based accounting firm, to settle charges related to the audit of Satyam.[87] The respondents consented to a censure and agreed to refrain from accepting new U.S.-based clients for a six-month period. The affiliates also agreed to establish training programs in accounting and securities laws for their officers, conduct a review of their auditing policies, and appoint an independent monitor to ensure reforms are timely and effectively implemented. Certain India affiliates also reached a settlement with the Public Company Accounting Oversight Board (“PCAOB”), and agreed to pay $1.5 million in additional penalties to the PCAOB,[88] which PCAOB described as its largest-ever civil monetary penalty. Indian authorities have also filed parallel criminal charges against two lead audit partners of one of the India affiliates.

B. Executive Compensation Clawbacks

The SEC has continued the use of its executive compensation clawback authority in 2011. As noted in the 2010 Year-End Report, Dodd-Frank expanded the reach of the Section 304 clawback provisions beyond CEOs and CFOs to also encompass any current or former executive of a restating company.

In March, the SEC settled an action against Ian McCarthy, President and CEO of Beazer Homes USA, one of the nation’s largest single-family home builders. Beazer was required to restate financial records for fiscal year 2006, which the SEC alleged were designed to artificially inflate Beazer’s income. The company was charged with manipulating land development and housing cost-to-complete accounts, along with recording some model home financings as sales. McCarthy himself was not charged with any of the alleged misconduct. Under the terms of his settlement, McCarthy reimbursed Beazer the full amount of his 2006 bonus package — over 40,000 restricted stock units, 78,000 restricted shares of stock, and $6.47 million in cash.[89]

C. Other Notable Accounting Cases

1. DHB Industries

The SEC filed charges in February against DHB Industries (now Point Blank Solutions), one of the largest suppliers of body armor to American law enforcement agencies and the U.S. military. It filed additional, separate charges against three outside directors and audit committee members, alleging that they facilitated the company’s fraud by “willfully ignoring numerous, significant red flags” that showed accounting fraud and the misappropriation of funds. The complaint alleges that three outside directors allowed management to manipulate the company’s gross profit, overstate inventory values and falsify journal entries. It further alleges that their “willful blindness” allowed DHB’s former CEO to divert $10 million from the company into a related entity he controlled, all via fraudulent transactions. Though DHB has settled the charges against it, the independent directors have not. For more information on this case, see our prior client alert, SEC Targets Directors Who Ignore Red Flags.[90]

The SEC also filed an action against former CEO Brooks and two other senior executives for their roles in the alleged fraud. In a parallel criminal case, Brooks and Sandra Hatfield, DHB’s former COO, were found guilty of securities fraud and obstruction of justice, among other charges, and await sentencing. Dawn Schlegel, DHB’s former CFO, pled guilty to related charges. The SEC’s civil action against the three executives is stayed pending criminal sentencing.

2. Powder River Petroleum

In April, the SEC settled several actions against Steven Hanni and Jeffery Johnson, accountants for Oklahoma oil and gas company Powder River Petroleum, arising from their roles in $43 million in improper revenue recognition from the sale of working interests in oil and gas leases to Asian investment firms.[91] The SEC alleged that the company failed to disclose that proceeds from the working interests were being used to fund payments it had previously guaranteed to earlier investors, that Powder River erred in reporting the working interests as revenue instead of borrowing, and that the company inflated its assets by including as revenue two leases it had ultimately failed to acquire.

Hanni and Johnson provided accounting and financial reporting services to Powder River. Johnson also served as Powder River’s CFO on a part-time basis during the relevant period. The SEC alleged that Hanni and Johnson failed to properly assess Powder River’s revenue recognition policies, despite being aware of the nature of the working interest payments. The SEC charged Johnson with causing Powder River’s false reports in the third quarter of 2007, year-end 2007 and the first-quarter 2008, and charged Hanni with causing the company’s misleading reports from year-end 2005 through the first quarter of 2008.[92] Johnson agreed to a five-year prohibition on serving as an officer or director of a publicly traded company. The SEC also filed charges against former Powder River CEO Brian Fox for his role in the company’s financial misstatements.[93]

3. Dohan + Company CPAs

In a continuation of the SEC’s investigation surrounding International Commercial Television (“ICTV”), described in the 2010 Year-End Report, the SEC imposed sanctions against Dohan + Company CPAs for a deficient 2007 audit of ICTV’s original and restated financial statements.[94] According to the SEC, Dohan + Company partners Steven Dohan and Nancy Brown were made aware of ICTV prematurely recognizing revenue from a drop-ship agreement with the Home Shopping Network (“HSN”), whereby ICTV recognized revenue upon HSN’s order of the product even though ICTV retained title until the product was sold by HSN to a third party. ICTV restated, and Dohan + Company gave a clean audit opinion on the restated financials. But subsequent auditors found additional revenue recognition errors, resulting in a further restatement. Dohan + Company agreed not to engage in new audits of public companies for 12 months and accepted a censure. Both Steven Dohan and Nancy Brown were individually sanctioned for their roles in the deficient audit.

4. Thor Industries and Dutchmen Manufacturing

The SEC settled an action in May against Thor Industries, a recreational vehicle company, and Mark Schwartzhoff, the former Vice President of Dutchmen Manufacturing–a Thor subsidiary–for improper record keeping and revenue recognition. The SEC alleged that Schwartzhoff, over a five-year period from 2002 to 2007, engaged in fraudulent accounting by concealing the cost of goods sold and falsifying documentation to overstate Dutchmen’s income by almost $27 million.[95] Thor agreed to a $1 million penalty judgment, without admitting the allegations, and Schwartzhoff paid fines of $399,000. In a separate criminal action filed in the Northern District of Indiana, Schwartzhoff pled guilty to a count of wire fraud and agreed to make restitution payments of nearly $1.9 million.[96]

[1] Robert Khuzami, Director, Division of Enforcement, SEC, “Remarks at SIFMA’s Compliance and Legal Society Annual Seminar” (SEC Mar. 23, 2011), http://sec.gov/news/speech/2011/spch032311rk.htm.

[2] Id.

[3] SEC Release for Rules Implementing the Whistleblower Provisions of Section 21F of Securities Exchange Act of 1934 (May 25, 2011), http://www.sec.gov/rules/final/2011/34-64545.pdf.

[4] See Gibson, Dunn & Crutcher Client Alert, SEC’s Initiative to Foster Cooperation–Perspective and Analysis (Jan. 14, 2010).

[5] Non-Prosecution Agreement between Carter’s, Inc. and the Securities and Exchange Commission (Dec. 17, 2010).

[6] SEC Press Release No. 2011-112, Tenaris to Pay $5.4 Million in SEC’s First-Ever Deferred Prosecution Agreement (May 17, 2011), http://www.sec.gov/news/press/2011/2011-112.htm.

[7] Id.

[8] Deferred Prosecution Agreement between Tenaris S.A. and the U.S. Securities and Exchange Commission (May 17, 2011).

[9] Federal Acquisition Regulation 9.406-2(b)(1) and 9.407-2(a).

[10] Remarks of Robert Khuzami at Securities Industry Financial Markets (“SIFMA”) Legal and Compliance meeting, June 25, 2011.

[11] SEC Press Release No. 2011-131, J.P. Morgan to Pay $153.6 Million to Settle SEC Charges of Misleading Investors in CDO Tied to U.S. Housing Market (June 21, 2011), http://www.sec.gov/news/press/2011/2011-131.htm.

[12] SEC Press Release No. 2011-132, Morgan Keegan to Pay $200 Million to Settle Fraud Charges Related to Subprime Mortgage-Backed Securities (June 22, 20111), http://www.sec.gov/news/press/2011/2011-132.htm; In re Morgan Asset Mgmt., Inc. et al. Admin Proc. No. 3-1387 (filed June 22, 2011), http://www.sec.gov/litigation/admin/2011/34-64720.pdf.

[13] See Chad Bray, U.S. Scores Convictions: Three Guilty in Insider-Trading Trial, Wall St. J. (June 14, 2011); SEC v. Arthur J. Cutillo, et al., No. 09-09208 (LAK) (S.D.N.Y. filed Nov. 5, 2009), http://online.wsj.com/article/SB10001424052702303848104576383463441609054.html.

[14] SEC Press Release No. 2011-53, Board Member of Goldman Sachs and Proctor & Gamble Charged in Insider Trading Scheme (Mar. 1, 2011), http://www.sec.gov/news/press/2011/2011-53.htm; In re Rajat K. Gupta, Admin Proc. No. 3-14279 (Mar. 1, 2011).

[15] SEC v. Longoria, et al., No. 11-CV-0753 (S.D.N.Y filed Feb. 3, 2011); see also Litig. Release No. 21836 (Feb. 3, 2011), http://www.sec.gov/litigation/litreleases/2011/lr21836.htm.

[16] SEC v. Skowron III, et al., No. 10-cv-8266 (S.D.N.Y. filed Nov. 2, 2010, amended Apr. 13, 2011); Litig. Release No. 21291 (Apr. 13, 2011), http://www.sec.gov/litigation/litreleases/2011/lr21928.htm.

[17] Litig. Release No. 21291 (Apr. 13, 2011), http://www.sec.gov/litigation/litreleases/2011/lr21928.htm.

[18] Litig. Release No. 21867 (Feb. 28, 2011), http://www.sec.gov/litigation/litreleases/2011/lr21867.htm; SEC v. Krantz et al., No. 0:11-cv-60432-XXXX (S.D. Fla. Feb. 28, 2011), http://www.sec.gov/litigation/complaints/2011/comp21867-directors.pdf.

[19] SEC Press Release No. 2011-61, SEC Obtains Settlement with CEO to Recover Compensation and Stock Profits He Received During Company’s Fraud (Mar. 3, 2011), http://www.sec.gov/news/press/2011/2011-61.htm.

[20] Id.; SEC v. McCarthy, No. 1:11-CV-667-CAP (N.D. Ga. filed Mar. 3, 2011).

[21] Robert Khuzami, Director, Division of Enforcement, SEC Remarks to Criminal Law Group of the UJA-Federation of New York (SEC June 1, 2011), http://sec.gov/news/speech/2011/spch060111rk.htm.